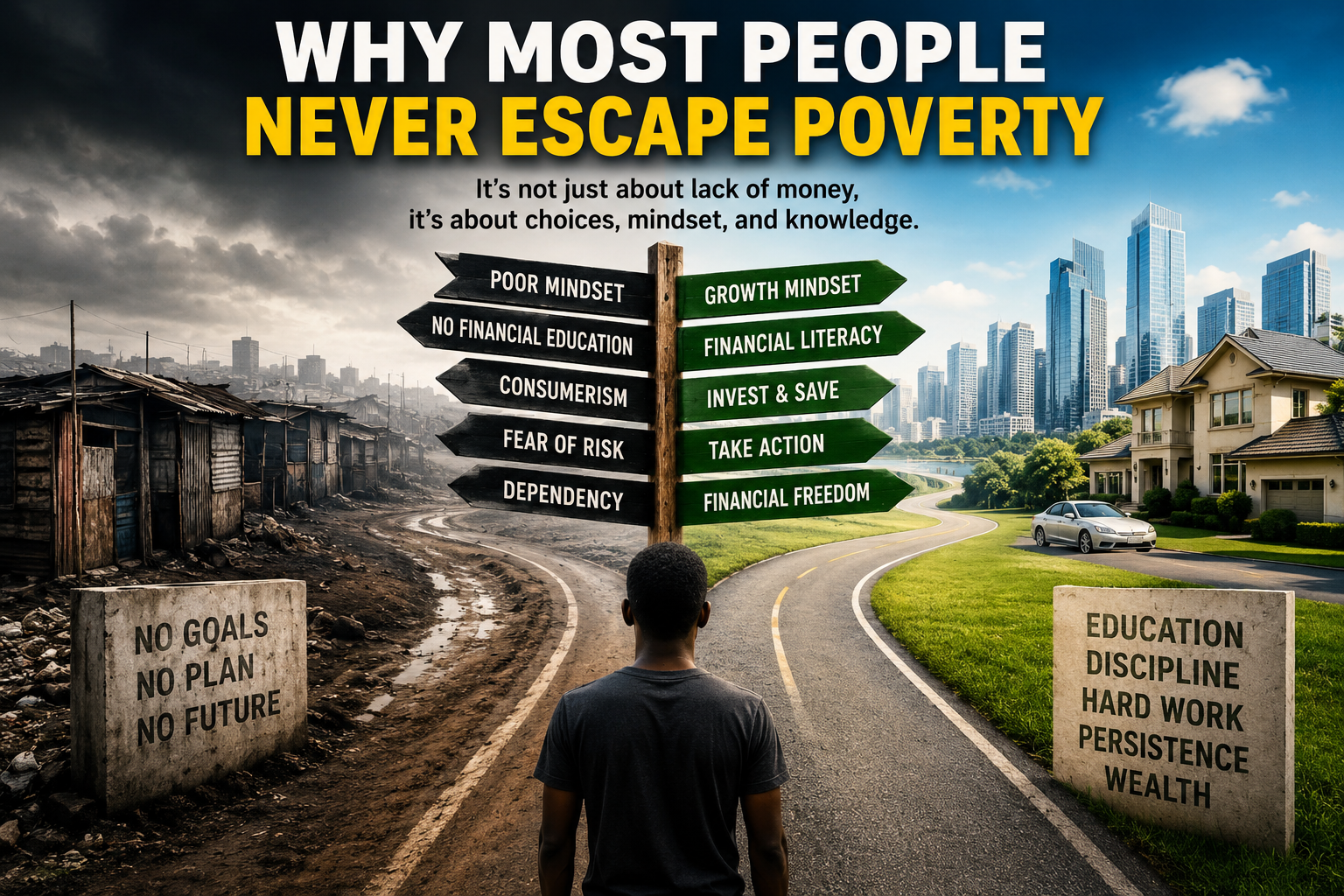

In today’s world, many people work hard, earn salaries, and stay busy every day, yet they still struggle financially. The truth is that poverty is not always caused by low income alone. In many cases, it is the result of unhealthy financial habits repeated consistently over time.

Financial success is often less about how much money you earn and more about how you manage what you have. Some habits quietly destroy wealth and prevent people from making financial progress, even in the modern information age, where opportunities are everywhere.

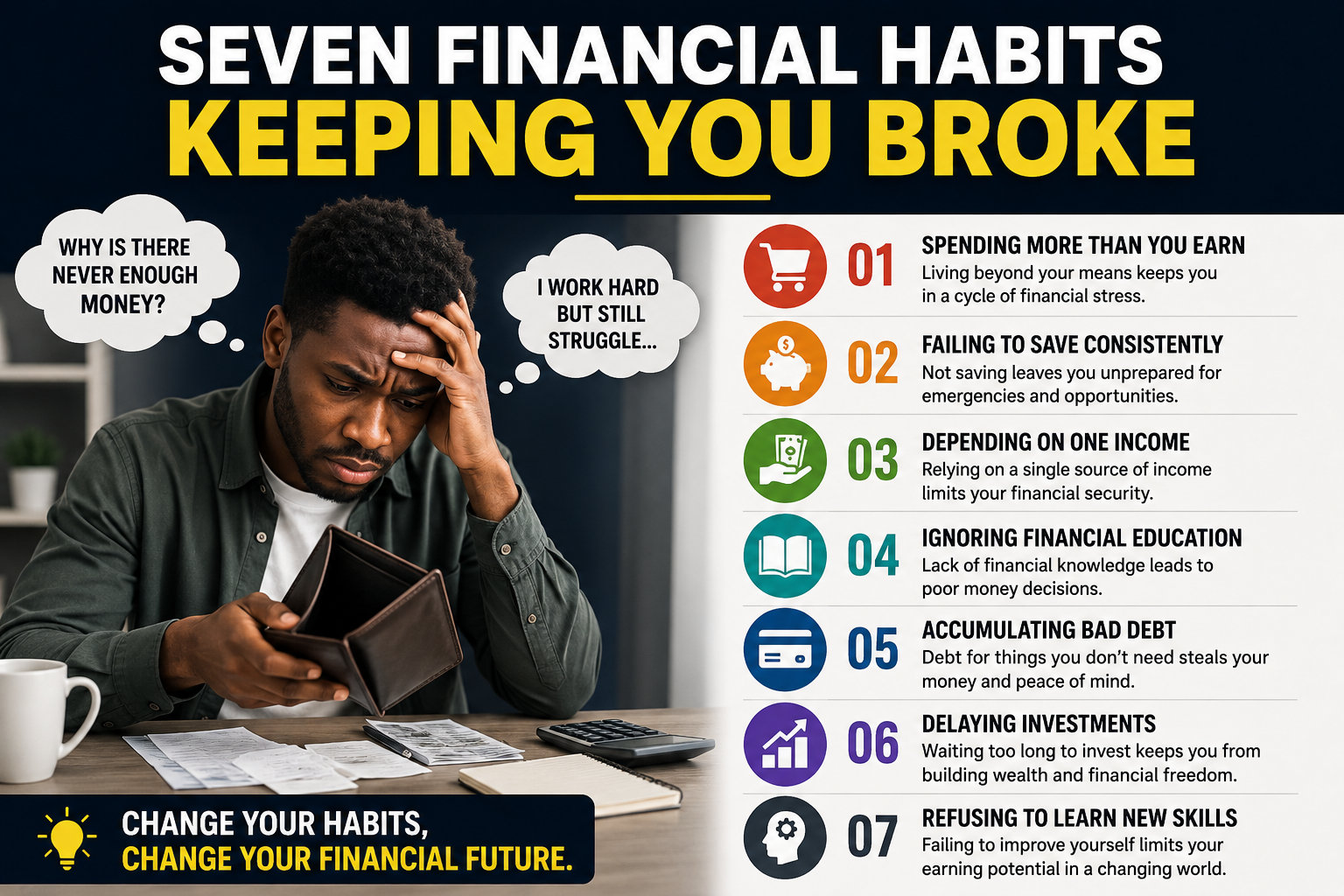

Here are seven financial habits that keep many people broke.

1. Spending More Than You Earn

One of the fastest ways to remain financially trapped is consistently spending more money than you make. Many people increase their spending immediately after receiving a salary increase or business profits. Instead of improving their financial position, they upgrade their lifestyles.

This habit is common in the social media era, where people feel pressure to appear successful online. Expensive phones, luxury clothing, parties, and unnecessary spending often consume money that could have been saved or invested.

A person earning a modest income but controlling expenses can gradually build wealth. However, someone earning a high salary yet living extravagantly may still be financially stressed.

Financial freedom begins when you learn to live below your means.

2. Failing to Save Consistently

Many people only save money when they have “extra” income left. Unfortunately, for most people, that extra money never comes.

Saving should not depend on convenience or mood. It should become a disciplined habit. Even small savings done consistently over time can create financial security and investment opportunities.

In the information age, unexpected events such as job losses, economic downturns, medical emergencies, or business challenges can happen suddenly. Without savings, people easily fall into debt or a financial crisis.

The habit of paying yourself first is one of the foundations of wealth creation.

3. Depending Only on One Source of Income

Another dangerous financial habit is relying entirely on one income source. Many people depend solely on salaries without building additional streams of income.

Modern economies are changing rapidly. Companies restructure, jobs disappear, and industries evolve. Depending on one paycheck alone can become risky.

Today, people can create additional income through freelancing, consulting, online businesses, digital products, investments, content creation, and side hustles. Yet many individuals refuse to explore opportunities beyond their primary jobs.

The wealthy often build multiple income streams, while financially struggling people usually rely on only one.

4. Ignoring Financial Education

Many people spend years in school but never learn practical money management skills. They know how to work for money but not how to make money work for them.

Financial ignorance leads to poor decisions such as uncontrolled debt, impulsive spending, lack of investment planning, and poor budgeting.

In today’s digital age, financial knowledge is more accessible than ever. Thousands of free resources exist online through books, podcasts, YouTube videos, courses, and financial blogs. However, many people spend more time consuming entertainment than improving their financial knowledge.

People who continually educate themselves financially are more likely to make smarter money decisions over time.

5. Accumulating Bad Debt

Not all debt is bad, but uncontrolled consumer debt can destroy financial progress. Many people borrow money to finance lifestyles they cannot truly afford.

Credit purchases, unnecessary loans, and impulsive borrowing often create long-term financial pressure. Instead of building assets that generate future income, many individuals accumulate liabilities that drain income monthly.

For example, buying expensive gadgets or luxury items with borrowed money may create temporary satisfaction but long-term financial stress.

Debt becomes dangerous when borrowed money is used for consumption rather than productive purposes.

6. Delaying Investments

Many people believe investing is only for the rich. As a result, they postpone investing until they feel financially comfortable. Unfortunately, waiting too long reduces the power of long-term wealth accumulation.

One of the greatest financial advantages anyone can have is time.

The power of compound growth allows small investments to grow significantly over many years.

A young person who starts investing small amounts consistently may eventually build more wealth than someone who starts later with larger amounts.

In the information age, investment opportunities have expanded beyond traditional systems. People can now invest in stocks, mutual funds, businesses, digital assets, and online ventures with relatively small starting capital.

The habit of delaying investments often keeps people financially stagnant.

7. Refusing to Learn New Skills

The world is changing rapidly due to technology and artificial intelligence. Skills that were valuable years ago may become less valuable over time.

Many people remain broke because they stop learning after formal education. They resist change and fail to adapt to new economic realities.

Today, high-income opportunities often favor people with digital, technical, communication, analytical, or entrepreneurial skills.

For example, individuals who learn graphic design, digital marketing, bookkeeping, coding, video editing, data analysis, or content writing can earn income globally from almost anywhere.

Meanwhile, people who refuse to improve themselves may struggle financially even while opportunities exist around them.

Learning is no longer optional in the modern economy. It is necessary for survival and growth.

Conclusion

Financial struggle is not always caused by a lack of opportunity. Often, it is the result of repeated habits that silently destroy wealth and delay progress.

Spending excessively, failing to save, ignoring financial education, depending on one income source, accumulating bad debt, delaying investments, and refusing to learn new skills are habits that keep millions trapped financially.

The encouraging reality is that habits can be changed. Small financial improvements made consistently over time can produce life-changing results.

In today’s information age, opportunities for financial growth are greater than ever before. Those who develop discipline, financial intelligence, and a growth mindset are far more likely to escape financial hardship and build lasting prosperity.